A growing number of payment decisions are no longer being assessed solely through static rules.

Across Canada’s digital payments ecosystem, financial institutions, payment processors, fintech platforms, and fraud teams are relying more heavily on systems that evaluate transaction behavior in real time, looking for unusual patterns that traditional monitoring tools may miss.

The shift is being driven by a practical challenge.

Payment activity has become faster, more frequent, and more fragmented across devices, channels, and platforms. Consumers move between mobile banking apps, digital wallets, online merchants, peer-to-peer transfers, and subscription services throughout the day. Meanwhile, fraud operations continue to adapt, often changing tactics faster than fixed detection rules can be updated.

As a result, discussions across the payments sector are becoming less focused on whether artificial intelligence should be used in fraud monitoring and more focused on how AI-assisted systems can support fraud operations at scale.

The technology itself is not the story.

The story is how payment infrastructure is evolving around it.

Traditional Fraud Rules Are Facing New Pressure

For years, many payment systems relied heavily on rule-based monitoring.

A transaction might be flagged because it exceeded a certain value, originated from an unusual location, or matched a known fraud indicator. These controls remain important and continue to form a significant part of fraud prevention frameworks.

The challenge is volume.

Modern payment ecosystems generate enormous amounts of transaction activity, much of it occurring continuously across multiple channels. Static rules can identify known risks effectively, but they are often less effective when fraud behavior changes rapidly or when legitimate customer activity becomes more complex.

A consumer traveling, switching devices, changing spending patterns, or adopting new payment methods may trigger alerts that appear suspicious even when no fraud exists.

That operational reality has increased interest in more adaptive monitoring approaches.

Transaction Intelligence Is Becoming a Larger Operational Function

Inside fraud operations teams, a growing focus is being placed on transaction intelligence rather than transaction screening alone.

Instead of evaluating individual payment events in isolation, many modern monitoring systems attempt to assess broader behavioral context.

Questions increasingly include:

- Does this transaction fit historical account behavior?

- Is device activity consistent with previous patterns?

- Has login behavior changed significantly?

- Are there unusual spending sequences?

- Does transaction timing align with normal usage habits?

The objective is not necessarily to block more transactions.

Rather, institutions are trying to make better decisions about which transactions deserve additional review and which can proceed without creating unnecessary friction for legitimate users.

That distinction is becoming more important as digital payment volumes continue to rise.

Behavioral Analytics Is Moving Closer to the Centre of Fraud Operations

Behavioral analytics has become one of the most discussed areas within payment risk management.

Rather than focusing exclusively on transaction details, these systems examine patterns of user activity across broader interactions.

This may include:

- login frequency

- device usage

- navigation patterns

- transaction timing

- account-access behavior

- payment history trends

Fraud teams often describe this approach as adding context rather than replacing existing controls.

A transaction that appears normal in isolation may become unusual when viewed against a wider behavioral profile. Conversely, activity that initially appears suspicious may be recognized as legitimate once additional context is considered.

That capability is particularly valuable in environments where payment activity occurs around the clock and where manual review resources remain limited.

This becomes even more relevant as payment speeds continue to accelerate.

Faster Payments Are Increasing the Importance of Real-Time Evaluation

The continued movement toward faster payment experiences is also changing fraud operations.

When transaction settlement windows become shorter, the time available for review can shrink dramatically.

That creates operational pressure.

Fraud teams still need to identify suspicious activity, but they often need to do so while maintaining customer expectations around speed and convenience.

This is one reason real-time transaction scoring has become a growing topic across the Canadian payments sector.

Rather than relying exclusively on post-transaction investigation, many organizations are exploring systems capable of assigning risk signals during the transaction process itself.

Perfect prediction is not the expectation.

The objective is to provide enough intelligence to support better decisions while payments are actively moving through the system.

Reducing False Positives Has Become a Business Priority

Fraud prevention discussions often focus on stopping fraudulent activity.

Yet many institutions now devote equal attention to reducing false positives.

False positives occur when legitimate transactions are incorrectly flagged as suspicious. For consumers, that can mean declined purchases, temporary account restrictions, verification requests, or delayed access to funds.

For businesses, the consequences can be broader:

- customer frustration

- abandoned transactions

- increased support costs

- operational inefficiencies

- reduced platform confidence

This is where AI-assisted monitoring is attracting attention.

Many payment providers believe more contextual risk evaluation can help distinguish between genuine fraud indicators and legitimate customer behavior, reducing unnecessary intervention while maintaining security standards.

The balance remains difficult.

Fraud teams are rarely rewarded for taking excessive risks. They are, however, increasingly expected to minimize disruption for legitimate users as well.

Automated Review Systems Are Changing Internal Workflows

Another development receiving attention involves fraud-review operations themselves.

Historically, large numbers of alerts often required extensive manual investigation.

Today, many organizations are introducing systems that prioritize alerts based on risk signals, helping analysts focus on transactions that appear most likely to require intervention.

This does not eliminate human oversight.

Many institutions continue to place significant emphasis on investigator review for higher-risk cases. What is changing is the volume of lower-risk activity that can be assessed automatically before reaching human teams.

As transaction volumes grow, workflow efficiency is becoming nearly as important as detection capability.

Fraud Monitoring Is Becoming Part of Broader Payment Governance

The discussion around AI-assisted fraud detection is increasingly intersecting with broader infrastructure conversations.

Operational resilience frameworks consider how fraud systems respond during periods of elevated activity.

Identity-verification initiatives examine how authentication signals can support transaction confidence.

Payment oversight discussions increasingly reference governance, monitoring, and operational controls.

These developments remain separate topics. Yet they are becoming more interconnected across modern payment ecosystems.

Fraud detection is no longer viewed solely as a security function operating on the edge of the system.

It is becoming part of the infrastructure itself.

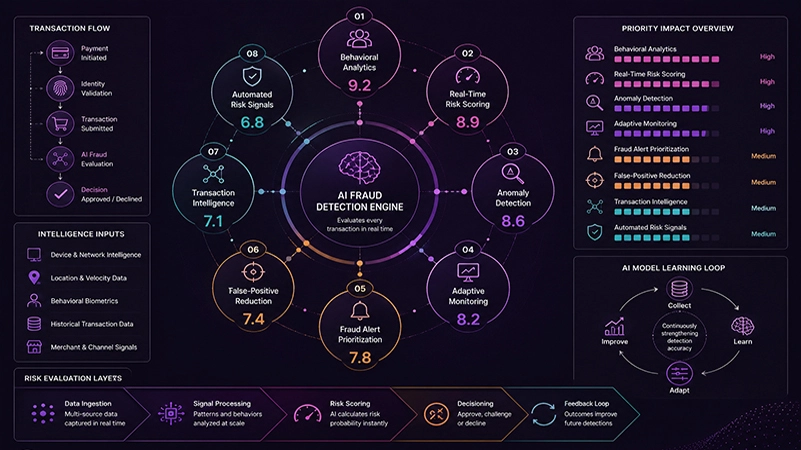

Table: Key Priorities Emerging in AI-Assisted Payment Fraud Operations

|

Area of Focus |

Operational Objective |

|

Behavioral analytics |

Identify unusual activity patterns |

|

Real-time transaction scoring |

Evaluate risk during payment processing |

|

Anomaly detection |

Detect activity outside expected behavior |

|

Automated review workflows |

Prioritize high-risk alerts efficiently |

|

False-positive reduction |

Reduce friction for legitimate users |

|

Adaptive monitoring systems |

Respond to changing fraud patterns |

|

Risk-signal integration |

Improve fraud decision-making consistency |

📊 Emerging Priorities in AI-Assisted Fraud Operations Across Canada

Subtitle:How behavioral analytics, anomaly detection, and real-time transaction scoring are becoming more prominent across Canada’s evolving payment ecosystem.

Source:Canadian payment-industry discussions, fraud operations analysis, fintech risk-management reporting, transaction-monitoring commentary, and digital payment infrastructure observations.

Conclusion

The growing use of AI-assisted fraud monitoring is changing how payment systems evaluate risk, even if most consumers never notice the underlying technology.

What users do notice are the outcomes: verification prompts that appear at unusual moments, payment alerts triggered by unfamiliar activity, temporary holds on higher-risk transactions, or account reviews designed to confirm legitimacy.

Behind those experiences sits a broader operational shift.

Payment ecosystems are processing larger transaction volumes, supporting faster payment flows, and managing increasingly sophisticated fraud environments. Traditional monitoring tools continue to play an important role, but many organizations are adding new layers of behavioral analysis, anomaly detection, and automated risk evaluation to support decision-making.

For Canada’s payments sector, the conversation is gradually moving beyond artificial intelligence as a technology topic.

The focus is becoming operational: maintaining transaction integrity, reducing friction for legitimate users, and managing risk across increasingly complex payment environments.

That conversation is likely to remain central as payment modernization, identity infrastructure, operational resilience, and fraud governance continue to evolve together.

FAQ

What is AI-assisted fraud detection in payments?

AI-assisted fraud detection refers to the use of advanced monitoring systems that help identify unusual transaction patterns, behavioral anomalies, and potential fraud risks during payment processing.

Why are payment providers adopting more adaptive fraud-monitoring systems?

Transaction volumes are increasing, payment experiences are becoming faster, and fraud tactics continue to change. More adaptive systems can help identify risks that may not match traditional rule-based patterns.

Does AI make fraud decisions automatically?

Not always. Many organizations use AI-assisted tools to generate risk signals, prioritize alerts, or support investigators rather than completely replacing human review.

What are behavioral analytics in payment systems?

Behavioral analytics examines patterns such as account usage, device activity, login behavior, and transaction habits to help identify unusual or potentially risky activity.

Why do consumers sometimes receive fraud alerts or verification requests?

These prompts often occur when transaction-monitoring systems detect activity that differs from expected account behavior and requires additional verification.

How does this connect to Canada’s broader payment modernization efforts?

As digital payments become faster and more interconnected, financial institutions are investing in technologies and operational processes that help maintain transaction security, continuity, and confidence across the payment ecosystem.