For much of the past year, Canada’s new payment service provider framework was discussed largely through the lens of registration deadlines and onboarding requirements. That conversation is starting to move elsewhere.

Across the Canadian fintech sector, legal teams, payment processors, wallet providers, and embedded finance platforms are now spending more time preparing for supervisory scrutiny tied to operations, governance, and safeguarding obligations.

The shift is subtle, but inside the industry it is becoming harder to ignore.operational failures disrupt digital transactions

Registration under the Retail Payment Activities Act (RPAA) was never designed to function as a simple licensing exercise. As the Bank of Canada continues shaping its supervisory approach, payment firms are beginning to confront a more demanding reality — one centred on operational accountability rather than administrative entry into the market.

For consumers, the implications reach beyond compliance terminology. The next phase of oversight is expected to influence how payment companies manage outages, protect user balances, monitor third-party risks, and respond when operational failures disrupt digital transactions.

Registration Was Only the First Layer

Early industry discussions around the PSP framework focused heavily on who needed to register and how the process would unfold.

That phase brought a wide range of businesses into clearer regulatory view: fintech startups, remittance providers, payment gateways, e-wallet operators, and certain merchant-service platforms that had historically operated with limited federal oversight.

Now the tone inside compliance circles is becoming more operational.

Law firms, consultants, and infrastructure advisers working with PSPs say the conversation has shifted noticeably in recent months. Less attention is going toward filing mechanics. More is going toward evidence, governance, testing, and documentation.

One recurring phrase appearing in compliance discussions is “show your work.” Not simply whether controls exist, but whether firms can demonstrate that those controls function consistently under real operating conditions.

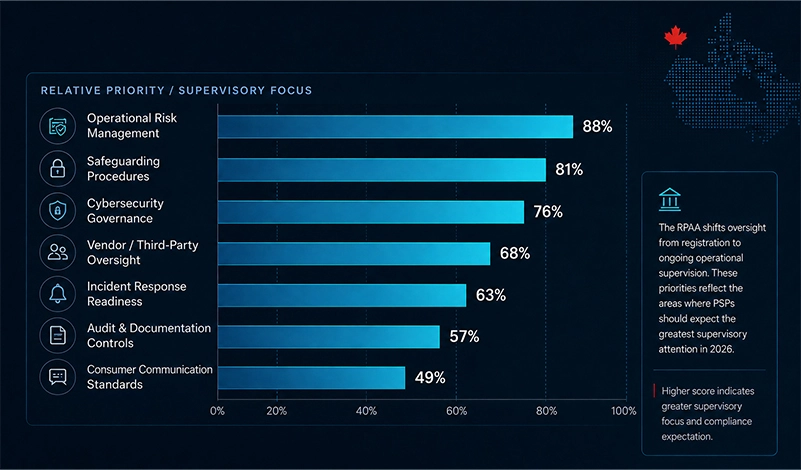

Operational Risk Is Becoming a Core Regulatory Focus

A clearer supervisory pattern is beginning to emerge around operational resilience.

Under the RPAA framework, payment service providers are expected to maintain risk-management and incident-response systems designed to reduce disruption risks and support recovery when problems occur.

That includes areas such as:

- cyber incident management

- third-party vendor oversight

- internal operational controls

- system availability

- record keeping

- business continuity planning

- data protection procedures

For many firms, these are no longer background compliance topics sitting inside policy binders. They are moving closer to core business infrastructure.

The direction is also broadly consistent with oversight trends already visible in other mature payments markets, particularly in Europe and the UK, where regulators have tied consumer trust more directly to operational resilience and governance standards.

In Canada, the discussion is becoming less about fintech expansion and more about infrastructure reliability.

Safeguarding Requirements Are Drawing Industry Attention

Another area attracting significant industry focus involves safeguarding obligations tied to end-user funds.

Under Canada’s emerging oversight framework, PSPs that hold funds on behalf of users are expected to maintain measures designed to reduce risks associated with insolvency, operational breakdowns, or misuse of funds.

That sounds straightforward in principle. Operationally, it can become far more complex.

Industry lawyers say many firms are now reassessing how customer balances are stored, separated, reconciled, and documented internally. Some companies already operate with trust structures and established banking relationships. Others are discovering that rapid growth created operational gaps that are harder to ignore once supervisory expectations become formalized.

There is also growing awareness that safeguarding discussions are no longer limited to legal departments. Treasury operations, finance teams, compliance officers, and infrastructure partners are all becoming part of the conversation.

Canadian PSPs Are Entering a More Document-Heavy Environment

Documentation is emerging as one of the defining themes of the new compliance phase.

Regulatory oversight increasingly depends not only on maintaining controls, but on proving that policies are reviewed, monitored, tested, and updated on an ongoing basis.

That shift is pushing many Canadian PSPs to expand internal compliance functions or seek external support in areas such as operational governance, cybersecurity oversight, and audit preparation.

|

Compliance Area |

Current Industry Focus |

|

Operational risk management |

Incident handling and continuity testing |

|

Safeguarding procedures |

Segregation and reconciliation controls |

|

Third-party oversight |

Vendor risk documentation |

|

Cybersecurity governance |

Internal reporting and escalation procedures |

|

Record retention |

Audit readiness and evidence management |

|

Consumer communications |

Transparency around service disruptions |

Smaller firms may feel the pressure most sharply.

A number of Canadian fintech companies were built around product speed and customer acquisition rather than layered governance processes. The newer supervisory environment is forcing some operators to formalize procedures that previously existed in fragmented or informal ways.

Not every company will adapt at the same pace.

The Oversight Shift Could Reshape Competitive Dynamics

The compliance transition may also alter competitive positioning across Canada’s payments sector.

Larger providers with mature governance structures are generally better positioned to absorb ongoing reporting, legal, and operational requirements. Smaller firms, meanwhile, could face rising costs tied to compliance staffing, documentation systems, and control testing.

Still, several analysts inside Canada’s fintech ecosystem argue that stronger oversight may ultimately strengthen confidence in non-bank payment services rather than suppress innovation.

That argument surfaces frequently in institutional discussions.

Payment reliability is increasingly treated as a trust issue, not just a technical issue. Outages, settlement failures, and operational incidents now attract broader scrutiny because digital payments sit so deeply inside everyday commerce.

The regulatory response is following that reality.

Canadian Financial Institutions Are Watching Closely

Banks, enterprise merchants, and payment processors are paying close attention to how the supervisory framework develops.

Many financial institutions rely on fintech partnerships for payment acceptance, embedded finance capabilities, merchant acquiring, and wallet infrastructure. A more active compliance environment may gradually influence partnership standards, vendor due diligence, and operational risk expectations across the sector.

Some observers expect compliance maturity to become a more visible commercial differentiator over time.

The questions institutions ask are also becoming more detailed:

- How are operational incidents documented?

- How quickly can systems recover from outages?

- What oversight exists for third-party vendors?

- How are customer funds protected internally?

- How often are controls tested and reviewed?

Those discussions point toward something larger taking shape inside Canada’s payment ecosystem: operational governance becoming part of market credibility itself.

📊 Canadian PSP Oversight Priorities Under the RPAA

How operational supervision is reshaping compliance expectations across Canada’s digital payments ecosystem in 2026

Source:Bank of Canada supervisory guidance discussions, Canadian fintech compliance commentary, RPAA implementation analysis, and payment infrastructure governance trends.

Conclusion

Canada’s PSP framework is entering a more consequential stage.

Registration established visibility into a rapidly expanding payments ecosystem. The next phase is focused more squarely on how firms operate behind the scenes — especially during disruptions, incidents, and periods of operational stress.

Inside the fintech sector, the conversation is becoming noticeably more practical. Governance testing. Safeguarding controls. Vendor oversight. Incident management. Documentation standards.

None of it generates the same attention as consumer-facing product launches. Yet these are the systems regulators increasingly associate with payment stability and public trust.

The broader transition is unlikely to happen all at once. But across Canadian fintech and payments infrastructure circles, the direction is becoming clearer: PSP oversight is moving beyond market entry and toward ongoing operational supervision.

FAQ

What is a PSP under Canadian regulation?

A PSP, or payment service provider, is a company that performs retail payment activities such as fund transfers, payment processing, digital wallet services, or payment initiation functions.

What role does the Bank of Canada play in PSP oversight?

The Bank of Canada is responsible for supervising certain payment service providers under the Retail Payment Activities Act framework, including registration administration and operational compliance oversight.

Is PSP registration enough to operate in Canada?

Not on its own. Registration is part of the framework, but firms are also expected to maintain operational risk-management systems, safeguarding controls, and internal compliance procedures.

What are safeguarding requirements for PSPs?

They are measures intended to help protect user funds held by payment providers. That can include segregation arrangements, reconciliation procedures, and operational controls designed to reduce risks tied to insolvency or misuse.

Why are operational controls becoming more important?

Because payment outages and operational failures now affect far more than fintech platforms themselves. Digital payments have become core infrastructure for everyday commerce, which places more regulatory attention on resilience and recovery planning.

Could stricter oversight affect smaller fintech firms?

Potentially yes. Some smaller operators may face heavier compliance and governance costs as supervisory expectations become more detailed and documentation-driven.